Market Moves & New Retirement Contribution Limits for 2026

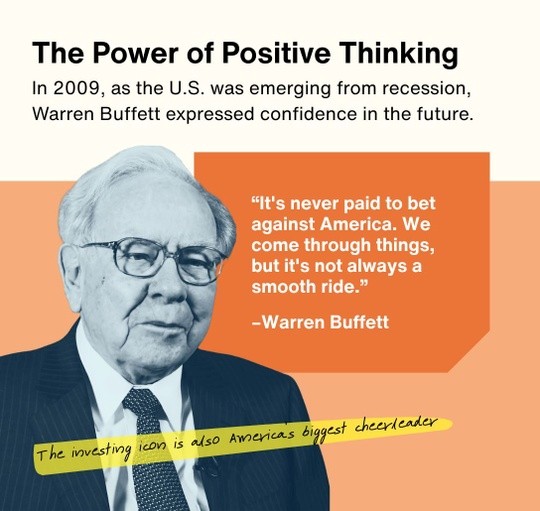

Warren Buffett’s quotes have provided clarity during confusion over the years. But his final act speaks louder than any expression. He did nothing.

As CEO, Buffett had nearly $400 billion in cash to spend in 2025. But he found no opportunities that he considered sensible. After he stepped down on Jan. 1, 2026, Buffett said he didn’t want to be sitting on so much cash. “At certain levels, cash is necessary, but cash is not a good asset.”

For individual investors, Buffett’s takeaway message is powerful: stick to your strategy. Don’t be impulsive and make an emotional decision. Allow your guiding factors to be your goals, time horizon and risk tolerance.

Markets Navigate Volatility While the Dow Reaches a New Milestone

Stocks were mixed last week, with broad gains on Monday and Friday bookending midweek selling pressure as investors digested earnings results from more than 100 S&P 500 companies.

The Standard & Poor’s 500 Index ended the week roughly where it started, slipping 0.10 percent, while the Nasdaq Composite Index declined 1.84 percent. The Dow Jones Industrial Average rose 2.50 percent. By contrast, the MSCI EAFE Index, which tracks developed overseas stock markets, rose 0.49 percent.

Dow 50,000

Stocks bounded out of the gate on Monday with the Dow leading a broad rise across all three major averages. Markets rose in anticipation of a big week for Q4 corporate reports.

Market sentiment quickly changed on Tuesday as anxious investors appeared to rotate out of technology names and into cyclical areas of the economy more likely to rebound with an improving economy.

News on Wednesday that private-sector job growth slowed in January added to investor anxiety. Stocks fell again on Thursday, with the S&P 500 briefly going negative year-to-date.

Then things turned around.

Stocks rebounded broadly on Friday as investors appeared to “buy the dip.” The Dow led, closing above the 50,000 level for the first time. The tech-heavy Nasdaq closed back above 23,000, while the S&P gained 2 percent. The latest University of Michigan survey showed consumer sentiment rose to its highest level in six months, helping buoy investor sentiment.

New Retirement Contribution Limits for 2026

The Internal Revenue Service recently released new limits for 2026. Although these adjustments won’t bring any major changes, there are some minor elements to note.

- Individual Retirement Accounts (IRAs)

IRA contribution limits are up $500 in 2026 to $7,500. Catch-up contributions for those over age 50 are up $100 to $1,100, bringing the total limit to $8,600. - Roth IRAs

The income phase-out range for Roth IRA contributions increases to $153,000-$168,000 for single filers and heads of household. For married couples filing jointly, the phase-out will be $242,000 to $252,000. Married individuals filing separately see their phase-out range remain at $0-10,000. - Workplace Retirement Accounts

Those with 401(k), 403(b), 457 plans and similar accounts will see a $1,000 increase for 2026, the limit rising to $24,500. Those aged 50 and older will now have the ability to contribute an extra $8,000, bringing their total limit to $32,500. Those aged 60, 61, 62 and 63 may enjoy a higher catch-up contribution of $11,250, raising their total contribution limit to $35,750. - SIMPLE Accounts

A $500 increase in limits for 2026 gives individuals contributing to this incentive match plan a $17,000 stoplight. Pursuant to the Secure Act 2.0, certain applicable plans have an increased limit of $18,100. - Gift and Estate Taxes

For 2026, the annual exclusion for gifts remains $19,000 per person. The estate tax exemption increases to $15 million for individuals and $30 million for those filing jointly.

Keep in mind that this update is for informational purposes only, so please consult with your CPA or tax advisor before making any changes in anticipation of the new 2026 levels. You can also contact our offices, and we can provide you with information about the pending changes.

Healthcare Costs in Retirement

In a 2025 survey, only 41% of all workers had calculated how much money they would need to pay for medical expenses in retirement. Being aware of potential healthcare costs during retirement may allow you to understand what you can pay for and what you can’t.

Health-Care Breakdown

A retired household faces three types of healthcare expenses.

- The premiums for Medicare Part B (which covers physician and outpatient services) and Part D (which covers drug-related expenses). Typically, Part B and Part D are taken out of a person’s Social Security check before it is mailed, so the premium cost is often overlooked by retirement-minded individuals.

- Copayments related to Medicare-covered services that are not paid by Medicare Supplement Insurance plans (also known as “Medigap”) or other health insurance.

- Costs associated with dental care, eyeglasses and hearing aids, which are typically not covered by Medicare or other insurance programs.

It All Adds Up

According to one study, the average total cost to cover healthcare expenses in retirement for a 65-year-old is $165,000.

Should you expect to pay this amount? Possibly. Seeing the results of one study may help you make some important decisions when creating a strategy for retirement. Without a solid approach, healthcare expenses may add up quickly and alter your retirement spending.

Preparing for healthcare costs in retirement starts now – not at age 65. Whether you’re still working, approaching retirement or already transitioning, it’s never too early (or too late) to put a strategy in place.

At Adams Brown Wealth Consultants, we help clients plan with confidence. Let us help you build a plan that keeps your care high and your stress low. Reach out today and take the first step toward a healthier, more secure retirement.

Source(s):

YCharts.com, Feb. 7, 2026. Weekly performance is measured from Monday, Feb. 2, to Friday, Feb. 6.

WSJ.com, Feb. 6, 2026

Investing.com, Feb. 6, 2026

CNBC.com, Feb. 2, 2026

EBRI.org, 2025